From Cluster Strategy to Vertical Integration — SoftBank's Push to Build a Chip-Power-DC Unified AI Empire

On March 24, it was reported that Arm is releasing its own AI server chip, and that Meta and OpenAI will adopt it. At first glance, this looks like a new product announcement in the semiconductor industry.

But if you see it as Arm — a SoftBank subsidiary — stepping beyond its traditional role as a “neutral IP licensor” to sell finished chips itself, the meaning of this news changes considerably.

Arm’s move is not just a new product launch. I see it as a signal that SoftBank, in the AI era, is trying to control not just AI models through its OpenAI investment, but the entire foundational layer — chips, data centers, and power.

Until now, SoftBank had pursued a “cluster strategy” through its Vision Fund, investing broadly in various startups and technology companies with AI as a central theme, trying to build a large ecosystem. But looking at the recent moves involving OpenAI, Arm, Ampere, SB Energy, and large-scale data center investments, that strategy is gradually changing shape. What SoftBank is trying to do now is not simply lining up promising companies side by side, but controlling the layers needed for AI to actually run, from top to bottom.

In other words, the Vision Fund era’s “cluster strategy” is evolving into a vertical integration strategy for AI infrastructure, centered on OpenAI and Arm, extending to data centers and power. I think the Arm chip news is one of the clearest signals of this shift.

What We Can Confirm as Fact

On March 24, 2026, Arm announced its first AI data center chip, the “Arm AGI CPU.” This means Arm is stepping beyond its position as an IP license provider — a “neutral designer” — to become a seller of finished chips.

According to Reuters, the chip will be manufactured on TSMC’s 3nm process, with mass production planned for the second half of 2026. Meta, OpenAI, Cloudflare, SAP, and SK Telecom are among the initial customers. Arm expects the chip to contribute $15 billion in annual revenue within five years.

What matters here is that Arm’s move does not stand alone.

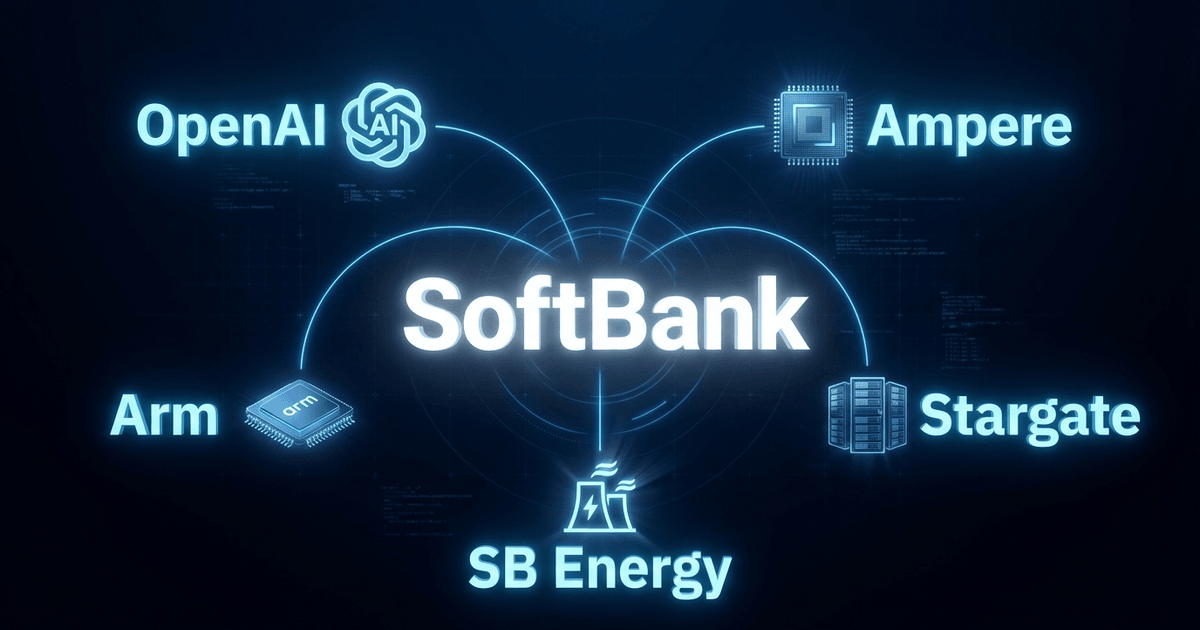

In March 2025, SoftBank acquired Ampere Computing for $6.5 billion. Ampere is a data center CPU company whose products are based on the Arm architecture. This means SoftBank now holds “design IP” through Arm and “server CPU implementation capability” through Ampere. It is natural to read this as a move to capture AI server value beyond GPUs — specifically in CPU and near-memory optimization.

SoftBank is also deeply involved in AI infrastructure itself, alongside OpenAI. In January 2025, OpenAI, SoftBank, and Oracle jointly announced “Stargate,” an AI infrastructure initiative worth up to $500 billion. Additionally, in January 2026, OpenAI and SoftBank each invested $500 million in SB Energy to build a 1.2-gigawatt data center in Milam County, Texas. SB Energy serves as the builder and operator. In other words, SoftBank is no longer just an investor — it is becoming the party that controls power and facilities.

In March 2026, further reinforcing this direction, Reuters reported that SoftBank and U.S. utility AEP are developing a 10GW AI data center on federal land in Ohio, integrated with 9.2GW of gas-fired power.

Japan’s investment amounts to roughly $33.3 billion, and SB Energy plans to invest $4.2 billion in grid reinforcement. At this point, SoftBank’s interest has clearly shifted from “investing in AI model companies” to “securing the power, land, substations, and server capacity needed to run AI models”.

SoftBank itself is not hiding this direction. Its annual report lists “AI chips,” “AI robots,” “AI data centers,” and “energy” as priority areas for the ASI era, to be pursued under the “Cluster of No.1 Strategy.” The joint AI agent business with OpenAI in Japan (“Cristal Intelligence”) and Stargate involvement are presented in the same context. This is not outside speculation — the company itself describes AI chips, data centers, and energy as a single strategic bundle.

What Has Changed

Some historical context is needed here. The SoftBank Vision Fund, launched in 2017, was designed to deploy massive capital into companies seen as promising for the AI era.

Its targets spanned ride-hailing, logistics, finance, e-commerce, semiconductors, telecommunications, and more. Masayoshi Son did not see these as disconnected investments — he viewed them as a “cluster” that would eventually interconnect.

In other words, rather than nurturing one specific company, SoftBank at that time was trying to broadly secure many leading companies and generate value from the entire network. SoftBank called this the Cluster of No.1 Strategy.

The idea was essentially a broad, horizontal, network-style dominance.

But now, SoftBank is transforming the same “cluster strategy” into a more physical, elite, vertically extended network. It is embedded in the model and application layer through OpenAI, in the chip layer through Arm and Ampere, in the power and data center layer through SB Energy and Stargate, and in the enterprise deployment channel in Japan through SB OpenAI Japan.

This is not the old structure of betting broadly on many startups.

This is a structure that threads a few critical assets vertically through the AI stack. If the Vision Fund era was “a portfolio lining up many promising startups,” the current era is “a portfolio that controls winning companies vertically.”

Arm’s Chip Entry Is Symbolic of This

What makes the Arm AGI CPU news symbolic is that Arm has stepped from being “a company that sells blueprints” to “a company that also sells finished products.” This naturally creates tension with existing customers like Nvidia, AWS, Microsoft, Google, and Qualcomm.

Indeed, Arm’s move is being perceived as a departure from its traditional neutrality.

But from SoftBank’s perspective, this is not so much a problem as it is the intent.

In an era where AI compute is scarce, licensing fees for designs alone are thin. Owning finished chips, server configurations, and the data centers that house them allows for much thicker margins.

Moreover, this chip is not meant to replace general-purpose GPUs of the Nvidia type.

The aim seems rather to be about securing inference-strong CPUs, as AI models commoditize and the competitive focus shifts from training to inference cost and operational efficiency.

Arm itself positions this AGI CPU as being for “agentic AI,” with Meta, OpenAI, Cloudflare, and SAP among the initial customers.

I think this is a very rational move.

The market for ultra-high-performance training GPUs has high barriers to entry, both technically and in terms of capital. The inference side, on the other hand, is more fragmented by use case and more open to custom designs and ASIC-like approaches.

Moreover, even without chasing peak performance, reducing dependence on external vendors and increasing internally manageable compute is economically rational for many companies. AWS’s custom chip strategy has shown exactly this path.

What SoftBank’s camp is aiming for is to control the inference space that GPUs alone cannot fill.

As demand for AI agents and multi-step inference grows, this space becomes more important. What is characteristic of Son is that rather than attacking Nvidia’s stronghold head-on, he is positioning in advance in a space that will grow in the future.

The Intel Investment

Here, the Intel investment should not be overlooked.

In August 2025, SoftBank invested $2 billion in Intel, becoming one of its major shareholders.

The Arm AGI CPU itself is currently planned for TSMC’s 3nm manufacturing, but the fact that SoftBank has also put capital into Intel suggests an intent not to depend solely on TSMC — a desire to also secure U.S.-based manufacturing capacity and advanced semiconductor supply.

At minimum, it is clear that Son’s vision does not end with design IP. He is trying to control the entire chain: designing chips, choosing where they are manufactured, where they are deployed, and what power runs them. In that sense, the Intel investment should also be seen as a supporting line of vertical integration.

About SB Energy

Another piece that should not be overlooked in SoftBank’s vertical integration is SB Energy. This is not simply a remnant of a renewable energy business. SoftBank has long been developing large-scale solar and storage projects in the U.S., but in the AI era, those assets have taken on new meaning as a way to secure data center power.

Renewable energy investments that previously seemed separate from the AI mainstream are now connected in a line with Arm, OpenAI, and data center investments.

SB Energy’s strength lies not just in investing in power plants, but in its ability to handle generation, storage, grid connection, financing, construction, and operations as an integrated package.

Competition in the AI era is no longer just about securing GPUs. Where you can secure sufficient power, on what land, and how quickly you can bring data centers online — these have become competitive advantages in themselves. Seen this way, SB Energy is the “power, land, and facilities” foothold for the SoftBank camp. If Arm and Ampere are the compute-side foundation, SB Energy is the physical infrastructure execution team.

What SoftBank is aiming for is not just investing in model companies. It is about controlling the entire foundation needed for AI to actually run — chips, power, and data centers. SB Energy’s existence makes this vision very clear.

My View

What I find important in this series of moves is that SoftBank is moving from being “an investor in AI companies” to something closer to “an operating holding company for AI infrastructure.” Its strength does not come from investing in OpenAI alone. It comes from owning Arm, acquiring Ampere, building power and data center capacity through SB Energy, entering the demand side through Stargate, and holding enterprise sales channels in Japan. If this formation is completed, SoftBank could hold a more stable share of the infrastructure layer, outside the volatility of AI application competition. AI models come and go, but chips, power, land, substations, cooling, and enterprise deployment do not change easily. That is where the economic rationale lies.

My point is that SoftBank is not heading in the Vision Fund direction of assembling many AI-related startups. Instead, it is building a portfolio that vertically integrates from chips to data centers to power, anchored by a few elite assets like OpenAI and Arm.

This is less about “investing in AI companies” and more about controlling the foundation on which AI runs.

I believe what SoftBank is aiming for is precisely such a vertically integrated AI empire. This thinking inherits the Vision Fund era’s idea of “enclosing promising companies as a cluster,” but shifts the implementation from a financial portfolio to infrastructure, semiconductors, and energy.

The cluster strategy has not disappeared. It has transformed into vertical integration backed by heavier assets. That is the essence.

An Alternative View

Of course, this vision carries significant risks. First, the capital burden is extremely heavy. SoftBank’s LTV stood at 20.6% at the end of December 2025, up from 16.5% three months earlier, according to Reuters, and the market is watching its future fundraising capacity closely. In March, reports emerged that SoftBank was considering borrowing up to $40 billion for its OpenAI investment. A strategy that takes on chips, data centers, and power generation can be enormous if it succeeds, but if market conditions deteriorate along the way, the balance sheet comes under heavy pressure.

Second, there is Arm’s positioning. If Arm sells its own chips, conflict of interest with customers is unavoidable. Co-existence is possible while the AI market is expanding rapidly, but if a recession or oversupply occurs, customers may reconsider why they continue to depend on a company that also supplies their competitors’ design foundation. Arm’s reduced neutrality is a revenue expansion opportunity in the short term, but also a long-term source of ecosystem friction.

Summary

If you look at SoftBank’s recent moves as isolated news stories — a large OpenAI investment here, a new Arm chip there — you lose the full picture. The essence is that the Vision Fund era’s cluster strategy is evolving, in the AI era, into vertical integration that connects chips, power, data centers, and enterprise deployment from top to bottom.

OpenAI is the demand center. Arm and Ampere are the compute resources. SB Energy and Stargate are the physical foundation — data centers and energy. On top of that, SoftBank holds enterprise deployment channels into the Japanese market.

What SoftBank is aiming for is not to pick one winner in the AI race, but to own the foundational layers whose value increases as the AI race itself expands. That is what I believe.

Join the conversation on LinkedIn — share your thoughts and comments.

Discuss on LinkedInRelated Posts

Stargate and SoftBank's Biggest OpenAI Bet: When a Grand AI Vision Meets Operational Reality

SpaceX IPO and the Question of Valuation: How to Price Starlink's Communications Infrastructure and SpaceXAI